uae-vatregistration.com

Mandatory vs Voluntary VAT Registration in UAE – Thresholds, Benefits & Risks (2026 Edition)

Mandatory vs voluntary VAT registration in the UAE explained (2026). Compare thresholds, benefits, and risks to choose correctly. Get expert advice today.

Gupta Group International

1/15/20265 min read

Mandatory vs Voluntary VAT Registration in UAE – Thresholds, Benefits & Risks (2026 Edition)

Mandatory vs Voluntary VAT Registration in UAE – Thresholds, Benefits & Risks:

Value Added Tax (VAT) remains one of the most significant aspects of tax compliance for businesses operating in the United Arab Emirates (UAE). Since its introduction in 2018, the UAE VAT regime has evolved to provide clarity, structure, and compliance flexibility for companies of all sizes. Whether you’re a startup, SME, or large enterprise, understanding mandatory vs voluntary VAT registration is a critical part of your tax obligations and strategic planning.

In this 2026 edition, we explore everything — from registration thresholds and legal requirements to benefits, risks, and strategic considerations — helping you navigate VAT registration with confidence and compliance.

What Is VAT in the UAE?

VAT in the UAE is a consumption-based tax levied on most supplies of goods and services. The standard rate has been 5% since 2018, and VAT is administered by the Federal Tax Authority (FTA) under UAE VAT Law. VAT is designed to standardize taxation across economic activities while allowing businesses to reclaim tax paid on eligible inputs.

Understanding VAT Registration:

VAT registration is the official process where a business obtains a Tax Registration Number (TRN) and becomes a “taxable person” under UAE law. This triggers obligations such as charging VAT on sales, filing periodic VAT returns, and maintaining accurate records.

Understanding whether your business needs to register — either mandatorily or voluntarily — hinges on specific threshold criteria and your commercial strategy.

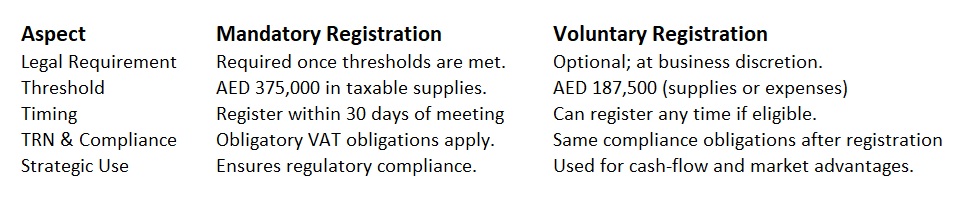

Mandatory VAT Registration Explained:

Understanding when a business must register for VAT is foundational.

1) When Is VAT Registration Mandatory?

According to UAE tax law, if a business exceeds a certain threshold of taxable supplies and imports, VAT registration becomes compulsory. Specifically:

A business must register for VAT when the total value of its taxable supplies and imports exceeds AED 375,000 over the last 12 months, or

It is expected to exceed this AED 375,000 threshold within the next 30 days.

If either condition is met, the company must complete registration within 30 days of the obligation arising to remain compliant.

2) Non-Resident Businesses

For non-UAE resident entities selling taxable goods or services within the UAE, the mandatory threshold doesn’t apply — they are required to register from their first taxable transaction unless another party in the UAE assumes VAT responsibilities.

Voluntary VAT Registration Explained:

While mandatory registration brings legal obligations, businesses that don’t meet the mandatory threshold may still choose to register voluntarily, provided they meet certain conditions.

Voluntary Threshold Criteria

A business can apply for voluntary VAT registration if:

Its taxable supplies, imports, or taxable expenses exceed AED 187,500 in the last 12 months, or

It anticipates exceeding this threshold in the next 30 days.

This option offers strategic benefits for businesses that are growing, have high costs, or serve B2B customers.

Key Differences: Mandatory vs Voluntary VAT Registration:

Detailed Thresholds for VAT Registration:

1) Mandatory Threshold – AED 375,000

This threshold includes:

All taxable supplies (standard-rated and zero-rated).

Imports into the UAE that would be taxable if supplied locally.

Exempt supplies such as certain local passenger transport and some financial services are excluded from the threshold calculation.

2) Voluntary Threshold – AED 187,500

This lower threshold allows smaller businesses to enter the VAT system, particularly beneficial for those with significant taxable expenses — even if they have not yet generated high revenue.

Benefits of Mandatory VAT Registration:

1) Legal Compliance:

Avoids penalties for late or non-registration — including fixed fines and backdated VAT liabilities.

2) Full Participation in VAT Ecosystem:

Once registered, businesses can:

✔ Charge VAT legally on their taxable sales.

✔ File VAT returns and remit tax.

✔ Maintain accurate VAT records — essential for audits.

3) Business Growth Preparedness:

Mandatory registration is a signal of business scale and maturity. It ensures readiness to serve larger clients, including government or corporate contracts.

Benefits of Voluntary VAT Registration:

Voluntary VAT registration brings strategic advantages beyond mere compliance.

1. Recover Input VAT:

Registered businesses can reclaim VAT paid on business purchases, improving cash flow for operating costs, assets, and services.

2. Enhanced Business Credibility:

A VAT registration number signals professionalism and regulatory conformity — helping attract larger corporate clients and investors.

3. Access to B2B Opportunities:

Many corporate or government clients prefer suppliers with VAT compliance, especially when they can reclaim VAT on purchases.

4. Early Investment Benefits:

Startups or companies with high setup costs can claim input tax credits early — even before reaching the mandatory threshold.

5. Compliance Readiness:

Establishing VAT processes early prevents last-minute rush and reduces error risk when a business eventually crosses the mandatory threshold.

Risks and Challenges of Both Registration Types:

Although voluntary registration is beneficial, both mandatory and voluntary registrants face similar obligations and risks.

1) Increased Administrative Burden:

Once registered:

Maintain detailed VAT records.

Issue VAT-compliant invoices.

File periodic VAT returns on time.

This can strain small businesses without robust accounting systems.

2) Pricing Impact:

Charging 5% VAT on sales may make products or services slightly more expensive for end customers — especially relevant for B2C businesses.

3) FTA Scrutiny and Documentation Requirements:

Voluntary registrants may need to provide substantial evidence (contracts, projections, invoices) to justify eligibility — especially when registering based on anticipated turnover or expenses.

Strategic Considerations for Small Businesses:

1) Evaluate Cash Flow Needs:

If your business has significant upfront costs, voluntary registration may help recover VAT earlier.

2) Monitor Turnover Regularly:

Tracking monthly and projected revenue helps avoid missing registration deadlines and incurring penalties.

3) Consider Client Base:

B2B businesses may benefit more from voluntary registration than B2C outfits, due to the ability of clients to reclaim VAT.

How to Register for VAT (Mandatory & Voluntary):

Registration in both cases follows the same FTA process via the EmaraTax portal:

Create and verify your EmaraTax account.

Complete the VAT registration application.

Upload all required documentation.

Submit and track the application through your dashboard.

The steps, requirements, and timelines are the same regardless of whether the registration is mandatory or voluntary — the only difference is the reason for applying.

Compliance Obligations Post-Registration:

Once registered:

Charge VAT at 5% on taxable supplies.

File VAT returns regularly (usually quarterly).

Keep VAT records for at least five years.

Remit VAT owed on time.

Compliance obligations are identical for both mandatory and voluntary registrants.

Penalties for Non-Compliance:

The FTA imposes considerable penalties for late or missed registration and non-fulfillment of VAT obligations:

Late Registration Penalty: AED 10,000.

Backdated VAT Liability: VAT may be charged from the date registration was required.

Interest on Unpaid VAT: Accrued with delays.

These penalties make timely and correct registration essential.

FAQs on Mandatory and Voluntary VAT Registration:

Q1. Can a business register voluntarily below AED 187,500?

No, the voluntary threshold is AED 187,500 unless the FTA accepts projected revenue evidence.

Q2. Do zero-rated supplies count toward thresholds?

Yes — both standard-rated and zero-rated supplies are included in threshold calculations.

Q3. How soon must I register after crossing thresholds?

Once mandatory conditions are met, registration must be completed within 30 days.

Conclusion:

Understanding the nuances between mandatory and voluntary VAT registration is crucial for regulatory compliance and strategic taxation planning in the UAE.

Mandatory registration ensures legal conformity and opens doors to new business opportunities once thresholds are met.

Voluntary registration offers strategic benefits — especially for startups and SMEs — in reclaiming input tax, enhancing credibility, and preparing for growth.

By comprehensively assessing your business’s turnover, expenses, client base, and long-term goals, you can make an informed VAT registration decision that aligns with both compliance and business performance.

© 2026 uae-vatregistration.com